Tax declarations will be filed through the Taxisnet system, the same way as the previous years. The late initial and amending declarations from 2015 and the following years will also be filed electronically.

In exceptional cases, the declarations can be filed by hand at the competent Public Revenue Agency due to a substantiated technical difficulty which cannot be solved, or if the competent supervisor of the Public Revenue Agency judges that there is an objective and real difficulty in filing the declaration electronically.

When do we submit a joint and when an individual declaration?

– The spouses file a joint income tax declaration if they are married when the declaration is filed.

– However, the spouses may file individual declarations if one of them expresses his intention to do so and declares said intention via the application of the Independent Authority of Public Revenue until February 28, 2020.

– Taxpayers who are common-law partners may also file a joint declaration (not compulsory).

– Spouses or common-law partners file individual declarations (without notification), when they no longer live together when the declaration is filed, or if one of the spouses is in bankruptcy proceedings or is subject to judicial support.

– An individual tax declaration is also filed if one of the spouses passes away.

Separation

To prove that the spouses are separated, the following is needed:

A copy of the petition for divorce or alimony or the minutes of the division of the joint property in case of divorce by mutual consent, or

If such does not exist:

Any evidence of the separation of the spouses e.g. separate residence which can be substantiated by filing:

– the lease agreement,

– Hydro bills, etc.,

– hospitality by mentioning it in his/her individual tax declaration

– free cession of residence,

which are considered real facts by the competent Public Revenue Agency.

A prerequisite of the above is that the Registry of the Public Revenue Agency is informed prior to filing the declaration.

The following must file a declaration:

– Anyone who has attained the age of 18 and has a real or taxable income.

– Anyone who has attained the age of 18 and is a self-employed professional.

– Residents living abroad only if they have a real income in Greece

– Minors who have an income from wages or pensions

– Any minor who has a business activity in his/her name must submit a hand-filled E3 form to the competent Public Revenue Agency, but is not obliged to submit an E1 form (the income is assessed in the name of the parent who exercises parental care).

The following do not have to file a declaration:

– Minors (apart from the cases mentioned above)

– Adults who have no real or taxable income

– Monks (not living in monasteries) for the net amount of their pension provided it does not exceed 9,500 Euro.

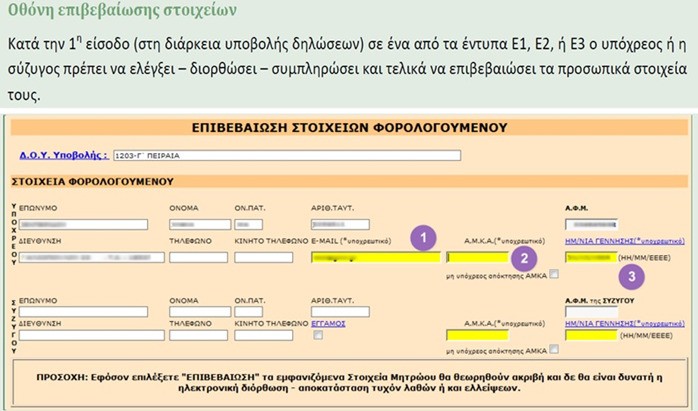

Table of confirmation of taxpayers’ information

For those submitting a tax declaration electronically for the first time, they must fill in the missing information.

As of this year, taxpayers do not need to write their IBAN for the return of taxes in every declaration that they submit, as the notification of the bank account number for payments (IBAN) to the Tax Administration will be made via an electronic Application/Solemn Declaration of the beneficiary at the website www.aade.gr in the TAXISnet section, and will be used for/connected to all tax payments.

Additionally, the taxpayer’s e-mail address must be declared and in the case of spouses, it must be filled in by both spouses.

In the individual declarations of married taxpayers, in the confirmation of the information, only the individual information is available.

Confirmation of information by tax residents living abroad

Tax residents living abroad are obliged to confirm their country of residence as well, as registered in the record containing the natural person’s information. If the taxpayer does not agree with the tax residence appearing in the confirmation of information table or the tax residence field is blank, he/she must amend/fill in said field.

In addition, taxpayers must fill in the relevant Tax Identification Number which they use in their country of tax residence and their full address abroad in Latin characters. If the taxpayer is not obliged to have a Tax Identification Number, then this field remains blank.

The above taxpayers must, in any case where it is requested, submit a certificate of tax residence to the competent Public Revenue Agency, in order to prove their country of tax residence.

Social Insurance Number (AMKA)

In the income tax declaration, the Social Insurance Number of the taxpayer and his spouse must be filled in. There are some exceptions where the taxpayers are not obliged to have a Social Insurance Number, namely:

– tax residents living abroad

– aliens and their dependants, who are exempt from the obligation to be insured with a local insurance provider, since they are insured with a foreign social insurance provider pursuant to a bilateral agreement, which means they cannot acquire a Social Insurance Number.

– taxpayers who, for reasons pertaining to sensitive personal data, do not wish to acquire a Social Insurance Number, neither for themselves or their dependants

– the employees of the Black Sea Trade and Development Bank

Tax Identification Number

The Tax Identification Number of the following must be filled in:

– any dependants over 18 years of age

– while for dependants under 18 years of age it is optional

If the minors are obliged to file a declaration, this must be indicated in table 8 and their Tax Identification Number must be filled in.

Provision of free accommodation

Anyone providing accommodation to dependants must declare them in Table 8 of form Ε1.

From the declaration, the fields 007-008 have been added, which are filled in by anyone providing accommodation to adults obliged to file a declaration, except those mentioned in the above table. The information which must be filled in is the Tax Identification Number of their guest and the months of provided accommodation.

In the case of married taxpayers who have informed of their decision to file individual declarations where one of the spouses does not have a co-ownership percentage to the main residence, whether it is proprietary, a free cession, or he/she participates as a tenant of the leased main residence, he/she fills, in the field 801, the spouse’s Tax Identification Number and, in the field 092 regarding hospitality, he/she selects, when filing the declaration electronically, the indication which has been added “co-habitation with spouse”.

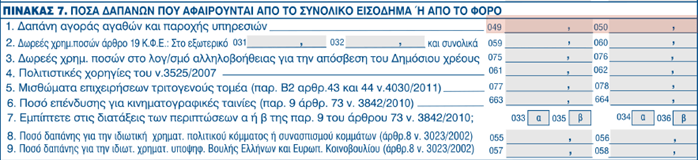

Declaring receipts

From the declarations of the tax year 2017, fields 049-050 were activated again. These fields contain the amounts for the preservation of the tax deduction (we mention below who is entitled to this tax deduction).

The taxpayer must have incurred these expenses in Greece or in a member-state of the European Union or the EAA and said expenses must have been paid by electronic means of payment, such as cards and means of payment using a card (debit or credit cards, pre-paid cards), via an account for the payment of Payment Service Providers of Law 3862/2010 (transfer of debit, orders for immediate credit, pre-authorized payments, bank or postal cheques), via e- banking, e-wallet etc., the minimum amount of which is determined as a percentage of the taxable income, according to the following scale:

Income | Percentage of minimum expense (progressive application) |

1 – 10,000 | 10% |

10,001 – 30,000 | 15% |

30,000 and above | 20% up to 30,000 Euro |

The above fields are blank; however, the electronic information will be provided. The taxpayers must calculate and fill in the amount of any specific expenses themselves and they must be able to prove these expenses to the tax administration.

If some of the documentation pertaining to the expenses for the preservation of the tax deduction have been submitted to the employer of the taxpayer or the insurance fund/ insurance company where he/she is insured in order for these expenses to be reimbursed, only the part of the expense which the taxpayer himself/herself has incurred is taken into account.

Examples of such expenses are any expenses for medicine, for the purchase of orthopedic items (splints, corsets, footwear etc.), expendable nursing materials, handicap aids (crutches, wheelchairs, bedrest mattresses etc.), special machinery (nebulizers, suction pumps, oxygen cylinders etc.), expenses for the transportation and the accommodation of the insured, hospitalization fees, expenses for nurseries etc., when they are not entirely covered by the employers, the insurance funds and the insurance companies, which can be used by the taxpayers, provided they do not constitute expenses which are not exempt pursuant to any other tax provision. In order to take these amounts into account, an attestation of the employer or the insurance fund or the insurance company is required containing the following information:

– The information of the person for whom the expense was incurred,

– The mode of payment and the total amount of the expense, for which the documentation was submitted,

– The number and date of the receipt for the provision of services or the receipt of retail sale on which the amount of the expense is mentioned,

– The amount of the expense covered by the employer or the insurance fund or company and

– The remaining amount of the expense which the taxpayer incurred.

If the assessment is issued in the year following the year during which the expenses were incurred, an amending declaration must be filed for the year during which the amount was paid or said expenses are declared for the year during which the assessment was issued.

ATTENTION: The following are exempt from the obligation to use electronic means of payment, but they are obliged to submit receipts for the equivalent value: taxpayers who are seventy (70) years old and over, namely, for the current year, those born until 31.12.1949, persons with a disability percentage of eighty percent (80%) and above, people under judicial support, taxpayers of the European Union or the EEA, pursuant to the stipulations of article 20 of Law 4172/2013, who are obliged to file a declaration in Greece and are subject to taxation according to the scale concerning salaried employment and pensions. Additionally, the same applies for the following categories of taxpayers:

- Public servants and employees serving abroad as well as tax residents of Greece who reside or are employed abroad

- Minors who are obliged to file an income tax declaration and are subject to taxation according to the scale concerning salaried employees and pensioners.

- Taxpayers who permanently reside in villages with a population of up to 500 residents and on islands with a population of less than 3,100 residents, according to the latest census, unless these are tourist destinations.

- Taxpayers who have no income from any category or who have an income only from capital and/or capital transfer gains and whose taxable income does not exceed the amount of 9,500 Euro.

- Taxpayers who are registered in the unemployment records of OAED, for the difference between their taxable and their total income.

- Taxpayers who receive Social Solidarity Income.

- Persons fulfilling their military service.

- Taxpayers in a situation of long-term hospitalization (more than 6 months).

- Third country citizens who apply for and/or are under the protection of the UNHCR and the European Commission.

- Taxpayers whose real income does not exceed six thousand (6,000) Euro, and whose taxable income does not exceed nine thousand five hundred (9,500) Euro.

Tax scales

Revenues have a different co-efficient depending on their source, same as last year.

Income from Salaried Employment – Pensions – Individual Business Activity

Income amount | Tax percentage |

0-20,000 Euro | 22% |

20,000-30,000 Euro | 29% |

30,000-40,000 Euro | 37% |

Above 40,000 Euro | 45% |

The tax from the above scale for salaried employees is reduced by 1,900 Euro for taxpayers without dependants for incomes up to 20,000 Euro. The reduction amounts to 1,950 Euro for taxpayers with one dependant, 2,000 Euro for two dependant children and 2,100 for three dependant children or more. It is reduced by 10 Euro for each 1,000 Euro income which exceeds 20,000.

Income from leases

Income amount | Tax percentage |

0-12,000 Euro | 15% |

12,001-35,000 Euro | 35% |

Above 35,000 Euro | 45% |

Rights

Income amount | Tax percentage |

Independently of the income | 20% |

Capital transfer –Interest

Income amount | Tax percentage |

Independently of the income | 15% |

Transfer of titles from onerous cause: stocks, shares, percentage of participation in companies, bonds, derivatives etc.

Dividends

Income amount | Tax percentage |

Independently of the income | 10% |

Prepaid tax

Prepaid tax is the amount equal to 100% of the tax which ensues only from the exercise of a business and agricultural activity as well as any difference in tax criteria, after deducting any taxes which were withheld and prepaid. Exceptionally for anyone filing a declaration for income from a business activity for the first time, the advance payment is equal to 50%.

For the calculation of the advance payment, taxes from income from other sources are not taken into account.

For anyone filing a declaration for the first time, the amount of the advance payment is reduced to half.

The advance payment which is assessed, is offset with the tax from the following tax year, independently of the category of income from which this tax ensues.

The prepaid tax is not assessed when:

– The prepaid tax is up to 30 Euro

If the income is reduced by over 25%, an application may be filed for the reduction of the prepaid tax until the end of September of the tax year during which the assessment was made and only concerns tax amounts which correspond to due instalments.

The application for the reduction is also filed when the taxpayer passes away, by the inheritors of the deceased, at the Public Revenue Agency within the same deadline of the tax year during which the assessment was issued.

If a declaration is not filed, the Tax Administration assesses the prepaid tax amount, based on the existing records for the latest tax year prior to which the filing of the declaration was omitted, provided it is ascertained that the taxpayer continues to have an income.

Tax criteria and tax co-efficient

The living criteria remain as is and are divided into two categories: assets and expenses.

Criteria concerning assets

Any difference between the assets and the real income is assessed in the declaration of the taxpayer. However, depending on the source of the income, the ensuing difference has a different tax co-efficient.

Scale for salaried employees and pensions

The difference of the criteria is subject to taxation based on the scale for salaried employees when:

- The income is solely acquired from salaried employment and pensions

- The largest or equal part of the incomes is acquired from salaried employment and pensions or

- There is no income from any category or

- The taxpayer is registered in the OAED unemployment records

- The taxpayer has acquired income solely from capital (e.g. rent) and/or capital transfer gain and his/her taxable income does not exceed the amount of 9,500 Euro

Scale for business activity

The tax criteria difference is subject to taxation according to the scale for business activity when:

- The income is acquired solely from a business activity

- The largest part of the income is not acquired from salaried employment and pensions.

Scale for agricultural activity

The tax criteria difference is subject to taxation according to the scale for agricultural activity when:

- The income is acquired solely from an individual agricultural activity or

- The largest part or equal parts of the income is acquired from an individual agricultural activity.

Note: As of the 2016 tax year the scales are common. The difference of whether the taxpayer will have a tax deduction or not, depends on the incomes.

Expense criteria

The expense criteria are added to the above criteria, including the purchase of property in 2018, such as:

– passenger vehicles

– recreational boats

– high value objects (above 10,000 Euro),

– houses,

– plots as well as any extension thereof

– the payment of loans,

– the issuance of loans and sponsorships,

– the purchase of businesses and company shares,

– any increase in the share or company capital,

– the purchase of investment products,

– expenses for private schools.

Joint bank accounts

In the cases of joint bank accounts in financial institutions (of any kind in Greece or abroad), the amounts of the interest on deposits which correspond to the real beneficiaries who are determined pursuant to real circumstances must be declared.

The supervisor of the competent Public Revenue Agency may, at his discretion, decide differently.

Rents

From the 2015 tax year and after, any non-collected income is declared in a special field for non-collected income from the leasing of real estate property of the income tax declaration and is subject to taxation for the year during which such was collected or will be collected.

The following must apply in order for the non-collected rents to not be calculated in the total taxable income, prior to the end of the deadline for the filing of tax declarations and in any case prior to the filing of the declaration:

– a payment order has been issued against the tenant or

– an order for the return of the leasehold

– an eviction decision from the courts or

– the adjudication of rents

– an eviction lawsuit has been filed against the tenant

– Especially, in the case where the tenant has declared bankruptcy, the submission of a copy of the table of notifications of debts on which the claim of the lessor/ sublessor appears is sufficient.

It should be noted that a clear copy must be submitted to the Public revenue Agency where it is verified and registered prior to filing the declaration.

This income is subject to taxation during the year and according to the amount which was collected.

Additionally, as of 1.1.2017, any income which is acquired from any short-term lease of property (via digital platforms), is considered income from real estate property, provided that the property which is leased is furnished and no service is provided apart from the provision of linen. If any other services are provided, this income is considered income from a business activity. Said income is declared, during the electronic filing, aggregately per property. Also, the gross income of the lessor from the leasing of a residence which is subleased on a short-term within the framework of the distribution economy via a digital platform by the lessee, is treated in the same way.

Capital consumption of previous years

For the calculation of the capital formed each year, the income which was taxed or legally exempt from tax, which was collected and which ensues from the offsetting of the assets and liabilities of the same year, is taken into account.

If, during a certain year, there is a negative balance, this negatively affects the assets of the previous years.

Also, these years must be consecutive up to the previous year from the year which the taxpayer invokes (current year).

Solidarity contribution

The scale for the calculation of the solidarity contribution for this year is as follows:

Income | Solidarity Contribution |

0-12,000 | 0.00% |

12,001-20,000 | 2.20% |

20,001-30,000 | 5.00% |

30,001-40,000 | 6.50% |

40,001-65,000 | 7.50% |

65,001-220,000 | 9.00% |

>220,000 | 10.00% |

Luxury tax

A luxury tax is imposed on the amounts of the annual objective expenses which ensue from the ownership or possession of high-capacity, private-use passenger vehicles, aircraft, helicopters and sailplanes, swimming pools, as well as private-use recreational boats of over five (5) meters, according to the income tax declaration and the other information at the disposal of the Independent Authority of Public Revenue.

The tax mentioned in this paragraph, which is imposed on the amounts of the annual objective expenses of the previous paragraph, is calculated as follows:

- For passenger vehicles of a capacity of one thousand nine hundred and twenty-nine (1,929) cubic centimeters to two thousand five hundred (2,500) cubic centimeters, the tax is equal to the product of the amount of the annual objective expense multiplied by a co-efficient of five percent (5%).

- For passenger vehicles of a capacity of two thousand five hundred (2,500) cubic centimeters and more, the tax is equal to the product of the amount of the annual objective expense multiplied by a co-efficient of thirteen percent (13%).

the imposition of this luxury tax excludes any private-use passenger vehicles of over ten (10) years of age from their first year of circulation in Greece or in an E.U./ EEA country, as well as private-use passenger vehicles of persons with disabilities, which are exempt from the registration tax. - For aircrafts, helicopters and sailplanes, the tax is equal to the product of the amount of the annual objective expense multiplied by a co-efficient of thirteen percent (13%).

- For swimming pools, interior and exterior, the tax is equal to the product of the amount of the annual objective expense multiplied by a co-efficient of thirteen percent (13%).

- For private-use recreational boars of over five (5) meters, the tax is equal to the product of the amount of the annual objective expense multiplied by a co-efficient of thirteen percent (13%).

The expense for the remuneration of the crew is not taken into account. The sailing boats and recreational boats which were constructed or are constructed in Greece exclusively from wood, such as trehantiri, varkalas, perama, tserniki, liberty, originating from the Greek maritime tradition, are exempt from said tax.

The luxury tax, is confirmed based on the declarations which are filed and appears in the notice of assessment for the calculation of the income tax.

Acquisition of property

Any acquisition of property from an illegal or unknown source or cause is considered as gain from a business activity, pursuant to the requirements stipulated by the Code of Tax Procedure.

This acquisition is not subject to taxation:

– provided the taxpayer can prove its real source

– and that it has been lawfully subject to taxation, or it is exempt from taxation according to special provisions.

If the proof is not satisfactory, any accretion of property is characterized and subject to taxation as income from a business activity, with a co-efficient of thirty percent (33%).

The accretion of the property may concern:

– movable or immovable property of any kind, such as plots, houses, vehicles, aircraft,

– bank deposits and any kind of securities (stock, coupons, bonds, mutual funds etc.),

which cannot be substantiated from the income declared by the taxpayer.

The change in the composition or the preservation of the property does not necessarily mean that there was in accretion.

For the substantiation of property accretion via the disposal of assets or via the acquisition of income which, in the past, did not need to be included in the income tax declaration of natural persons, either because it was tax-free or taxed in a special manner (e.g. interest), the proper legal documentation must be submitted.

Dividends

A dividend is the distribution of gains, originating locally or abroad, from:

– listed or non-listed shares

– establishment titles

– company shares from Limited Companies or Private Companies

– the participation in personal companies, joint ventures and other legal entities

– the pre-dividends distributed by limited liability companies (S.A.)

– the temporary gains delivered to shareholders

– interest from preferential shares

– the overperformance of investment in the mathematical reserves of insurance companies

– the distribution of gains from trusts

– off shore company gains

– the remuneration paid under any form to the members of the Board of Directors, the managers and the employees from the gains of the legal person or the legal entity based on the balance sheet.

A 10% tax is withheld from and rendered by the taxpayer receiving the above dividends, apart from some examples such as:

– maritime dividends

– intragroup dividends

– dividends for UCITS established in Greece or in another member-state of the European Union or in an EEA/EFTA state.

As of 01/01/2014, the taxpayers-natural persons who are tax residents in Greece and acquire dividends abroad, do not pay on their own the tax on the dividends (presenting themselves at the Public Revenue Agency), whether these are imported in Greece or remain abroad. They must, however, include them in their annual income tax declaration, in which all income must be mentioned and keep the required documentation with its official translation in their records.

If a tax has been withheld from a mediating financial institution, this tax shall be declared in the tax declaration of the natural persons and it will be offset with the corresponding tax.

The time of acquisition of the income from dividends originating abroad, is considered the time it was paid to the beneficiary, via a credit of the taxpayer’s bank account or in any other way.

Assessment of declarations

Α. Natural Persons

The Directorate of Electronic Governance (DILED) of the Independent Authority of Public Revenue (AADE) regarding declarations which were filed electronically, issues:

– the Acts of Administrative Determination of the Tax (notice of assessment), which constitutes and confirms the debt or claim of the taxpayers and notifies them of such. From the 2018 tax year onwards, in the case of spouses, two notices of assessment will be issued. One for each spouse or common-law partner. If, according to the assessment, one of the spouses has a credit, it will not be offset with the assessment of the other spouse.

Taxpayers, may print the act of administrative determination of the tax from Taxisnet (notice of assessment), using their access codes. In the case of spouses, each must access the system with his/her own codes to print his/her notice of assessment. If the spouse does not have any access codes to the taxisnet system, then the notice of assessment of said spouse shall be printed using the other spouse’s codes.

– If an audit of the documentation of the initial or amending declarations which are filed electronically is judged necessary, the taxpayer will be called to the Public Revenue Agency and he/she must submit such documentation within 5 working days. After expiry of such deadline, the declarations are assessed by the Public Revenue Agency, which deletes or corrects, where necessary, the amounts which lead to a tax exemption, deduction or relief of the declared income or tax reduction, which are not covered by the electronic files nor has the proper documentation been submitted in physical form and then the Acts of Administrative/ Corrective determination of the tax are issued.

– the acts of administrative determination of the tax are issued and sent to the taxpayers by the Public Revenue Agency which assessed the declaration.

– If, when filing the declaration, there is no electronic information regarding the declared income and taxes, the documentation is sent by registered mail to the DILED or are received by the Public Revenue Agency, on a case to case basis.

The taxpayer must mention all of his/her income in the declaration:

– independently of the taxation means, and

– any income exempts from tax.

For any income taxed independently or in any other way, the withheld or paid tax is also mentioned depending on the case.

Based on the electronic files sent to the DILED,

– either some of the income categories are pre-filled (such as salaried services, pensions etc.) and the withheld tax un the relevant field of the tables in the declaration,

– either the taxpayers are informed via a table of their income amounts as well as the other information of the declaration (e.g. loans),

– either the withheld tax are been pre-filled (business activity).

When the fields of the declaration are filled in with the income-taxes which were paid in Greece or abroad without any electronic information, the taxpayers must submit:

– the required documentation to the competent Public Revenue Agency or the DILED to be audited, in order to complete the assessment of their declaration.

For the amending income tax declarations, the initial declarations of which was filed online, the documentation which the taxpayer submits will be:

– only the documentation which pertains to the reason which is invoked for the amendment of their declaration and not the documentation pertaining to the overall declaration.

Tax payment

Income tax can be paid (according to current information):

– in three (3) equal bimonthly installments, of which the first must be paid by the last working day of the month of July and each of the following installments by the last working day of the months of September and November.

The tax settlement is independent of the date when the tax declaration was filed.

In cases where the declaration is filed within the required time period in written format at the Public Revenue Agency or is filed within the required time period electronically via the internet and is forwarded to the Public Revenue Agency for an audit of the documents, the payment of the tax is made in three equal bimonthly installments, of which the first must be paid by the end of the month following the assessment.

For the declarations which are filed late the three (3) installments also apply, with the lawful interest.

– their calculation will begin at the deadline for the payment of the installments stipulated by the law, namely in July, November, September.

– especially for declarations which are filed late and are audited by the Public Revenue Agency, the time between the filing of the declaration and its assessment by the Public Revenue Agency is not taken into account.

For amending income tax declarations which are filed:

– by salaried employees or pensioners with retroactive salaries or pensions from previous years, as well as

– taxpayers receiving agricultural subsidies from the OPEKEPE for previous years,

these declarations will be accepted without fines until the end of the tax year in which the attestations of remunerations or pensions or the relevant attestations from the OPEKEPE were issued, depending on the case.

The interest for delayed payments is calculated in the case of the delayed payment of the income tax. The interest does not constitute a sanction (fine) but is calculated due to the delay in payment of the debts.

The calculation of the interest begins on the following day after the expiry of the legal payment deadline. The interest rate for the calculation of the interest currently amounts to 8.76 percent annually (0.73% monthly).

The amount which is due pursuant to the act of administrative determination of the tax is not assessed, provided it does not exceed a total of thirty Euro for both the taxpayer and his spouse.

The tax amount which ensues pursuant to the act of administrative determination of the tax which is under five Euro for both the taxpayer and his spouse is not returned.